A new Qontigo report1 takes a comprehensive look at the market for ‘smart beta’ funds tracking factor strategies, to assess their prowess in boosting returns and their capacity as money inflows grow.

The study by Frank Siu, Executive Director of Quantitative and Multi-Asset Solutions at Qontigo, looked at exchange-traded funds (ETFs) tracking equity smart beta and factor investing, and listed around the world. By considering changes in their constituent weightings during periodic rebalancings, he estimated the transaction costs of trading and rebalancing the portfolios of each factor strategy. Costs were then compared against the factor risk premia associated with these ETFs, using the Axioma Equity Factor Risk Model.2

For all but two of 14 strategy types, the average factor premium exceeded the average rebalancing cost, the study found. The exceptions were growth and low liquidity. Interestingly, while momentum strategies are the costliest to trade, they also offer the most upside and growth potential.

Break-even

From there, Siu sought to establish at what level of assets will any given factor strategy cease to be profitable, by extrapolating the ‘break-even capacity’ where rebalancing costs offset the factor risk premia.

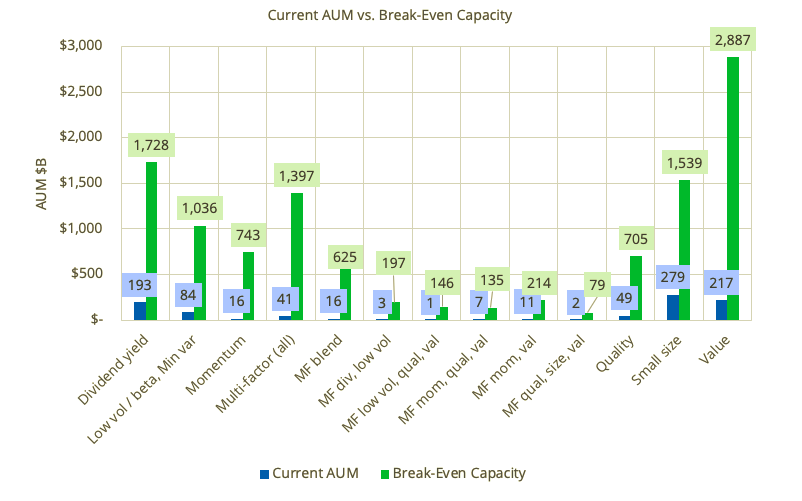

Exhibit 1, from the report, shows the break-even capacity level. In most cases, factor strategies are only at a fraction of their maximum capacity.

Exhibit 1

“We find that the market of smart beta strategies capturing equity factors has room to grow, and rebalancing costs are not expected to exceed factor premia for some time,” Siu wrote.

Enhancing results

“There is, however, space for innovation, particularly in methodological advances to more efficiently harvest factors and control liquidity,” he added. “Improvements in these areas could lead to even higher capacity for factor investing overall.”

One of those advances would be to address and improve portfolio liquidity, Siu argues. The recently launched STOXX® Factor Indices aim to maximize factor exposure while maintaining limits on liquidity, risk and diversification.

To gauge the potential impact of such optimized strategies on the capacity of smart beta, Siu repeated the earlier break-even capacity analysis but now assuming that the STOXX Factor Indices have a 20% share of the current smart beta ETF market.

Performing this simulation resulted in break-even capacity sizes that were either similar or higher in most instances. Additionally, inclusion of STOXX Factor Indices raised the factor premia being harvested in all categories except one. This is evidence that these are potentially more efficient vehicles for accessing factor risk premia than most current product offerings, the author wrote.

Growing assets

Smart beta and factor risk premia products have attracted strong flows in recent years as they are often viewed as a robust, transparent, and economical alternative to passive index strategies and active management alike. ETFs targeting equity factor strategies have risen almost fivefold over the past decade to top $1.2 trillion in assets under management, according to the study.

With smart beta’s popularity continuing, insight into the strategy’s cost-to-benefit relationship will be of interest to many investors. And as providers work to improve the efficacies of factor-based strategies, the findings in this study point to a positive picture for the sector in the near future. We invite you to read the full report here.

1 Siu, F, ‘Where is There Room to Grow? Assessing the Capacity of Factor Investing Strategies,’ Qontigo, September 2020.

2 For each factor strategy type, the study specifies the relevant target factor(s) based on style factors in the Axioma Worldwide Equity Factor Risk Model (AXWW4).