By Yurong Gu, Quantitative Multi Asset Solutions, Qontigo

Qontigo is introducing the STOXX® ESG-X Factor Indices, which combine the power of factor investing with sustainability principles.

The new index family is built up applying Axioma Factor Risk Models on environmental, social and governance (ESG)-compliant versions of STOXX benchmarks. It follows on the successful launch in January this year of the STOXX® Factor Indices, which offer robust factor definitions, explicitly targeted exposures and tradability, on flagship STOXX market-capitalization-weighted indices.1 The new STOXX ESG-X Factor Indices apply the same methodology on the universe of STOXX® ESG-X Indices, ESG versions of established benchmarks that were designed based on the responsible policies of leading asset owners.2

Both the standard Factor and ESG-X Factor families include five Single-Factor indices — value, quality, momentum, low risk and size — and a Multi-Factor index combining all five signals, for the Europe, Asia-Pacific, US, Japan and Global markets.3

Different pool of stocks

The primary difference between these two offerings is in the benchmark universe. The STOXX ESG-X universe is a filtered version of that of the STOXX benchmarks. This affects both the eligible pool of stocks and the benchmark used for the constraints in the index methodology. The exclusion criteria consist of a norm-based screening (Global Standards Screening4), as well as a product-involvement screening (controversial weapons, thermal coal and tobacco), based on data from Sustainalytics.

Analyzing performance and factor exposure

This blog post seeks to analyze, firstly, what effect on performance the implementation of exclusionary screens has on the benchmarks as well as on factor-based portfolios. Secondly, we’ll look into how a reduced universe impacts the target factor exposures of the STOXX ESG-X Factor Indices relative to the standard (non-ESG) Factor Indices.

ESG-X vs. parent benchmarks

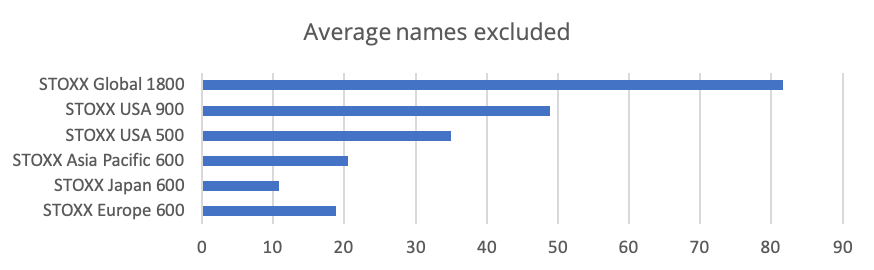

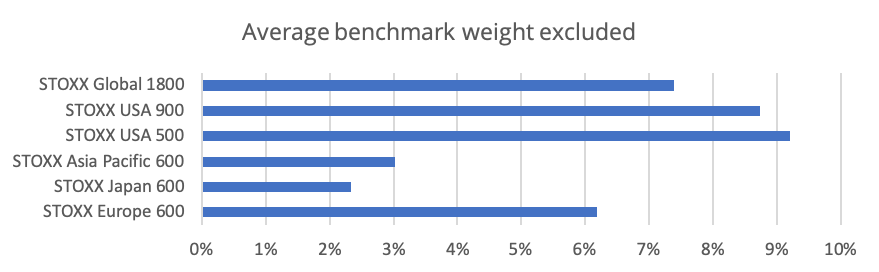

First, how different are the standard ESG-X indices from their parent benchmarks? The removed names and benchmark weights excluded vary by region (Exhibit 1). For example, the ESG-X screenings have excluded, on average, under 8% of the STOXX® Global 1800 Index’s weight.

Exhibit 1 – Exclusions by names and market capitalization

Source: Qontigo, March 2012 – March 2020.

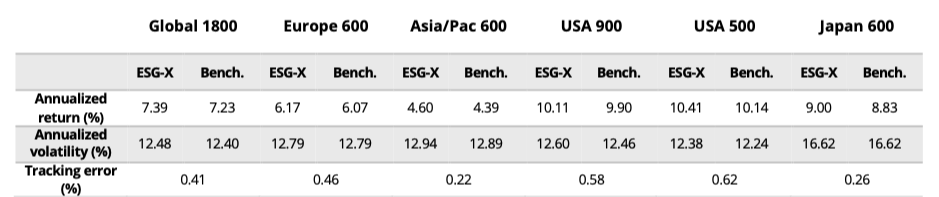

Exhibit 2 shows that the return and risk characteristics of the ESG-X indices and their parent benchmarks are not materially different, and that the tracking errors between them are small.

Exhibit 2 – Performances of ESG-X indices and parent benchmarks

ESG-X vs. standard factor indices

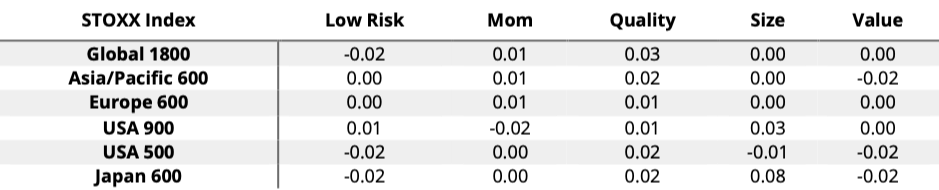

Next, we turn our attention to comparing the target factor exposures between the STOXX ESG-X Factor Indices and the standard STOXX Factor Indices. When looking at the target factor exposures for both Multi-Factor and Single-Factor indices (Exhibit 3), the differences are minimal, except for the Value factor index in the Asia/Pacific 600 and Japan universes. For example, the STOXX® Japan 600 ESG-X Ax Value Index is less exposed to the target factor (value factor) than is the STOXX® Japan 600 Ax Value Index by 0.08 standard deviations.

Exhibit 3 – Difference (ESG-X factor index minus standard factor index) in target factor exposure (Z-scores)

The target composite factor in Multi-Factor strategies is constructed by equally weighting all five single factors.

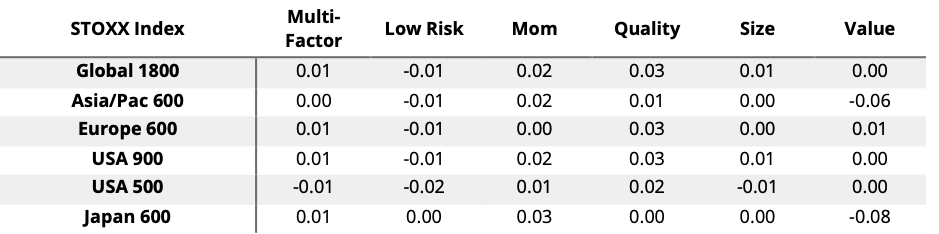

Exhibit 4 breaks down the difference in composite factor exposures (first column in Exhibit 3) to differences in five individual factors.

Exhibit 4 – Differences (ESG-X factor index minus standard factor index) of factor exposures (Z-scores) in multi-factor strategy

Performance

Finally, we observe insignificant differences in the performance of ESG-X factor and standard factor indices (Exhibit 5).

Exhibit 5 – Realized returns of ESG-X factor and standard factor indices

A deeper dive into Europe single-factor indices

As of March 2020, 21 names in the benchmark STOXX® Europe 600 Index were not eligible for the STOXX® Europe 600 ESG-X Index, and, hence, were not included in all the ESG-X factor indices derived from this ESG-X benchmark universe.

Only one excluded name was held in the standard Quality factor index (STOXX® Europe 600 Ax Quality Index): Uniper (Utilities), at a weight of 0.24%. Its target factor exposure is ranked 21st among the 600 benchmark constituents. Apart from this stock, all the remaining 20 excluded names have pretty low exposure to the quality factor with an average rank of 406 (out of 600). This, to some degree, is reminiscent of some practitioners’ findings that ESG and quality are related. Moreover, we note in Exhibit 3 that the ESG-X Quality index achieved slightly higher quality exposure than the standard Quality factor index in all six regions.

The standard Momentum factor index (STOXX® Europe 600 Ax Momentum Index) held two of those 21 excluded names: Novartis (Health care) and Airbus (Industrials), with a total weight of 1.78%. However, their target factor (momentum) exposures are both in the lower half of the universe.

As for value, the standard Value index (STOXX® Europe 600 Ax Value Index) held five of the excluded names: Novartis (Health care), British American Tobacco (Consumer goods), Volkswagen (Consumer goods), Leonardo (Industrials) and KGHM Polska Miedz (Basic materials). The total weight of these names is 14.81% and their contribution to the target factor (value factor) exposure is 0.05 (total 0.69).

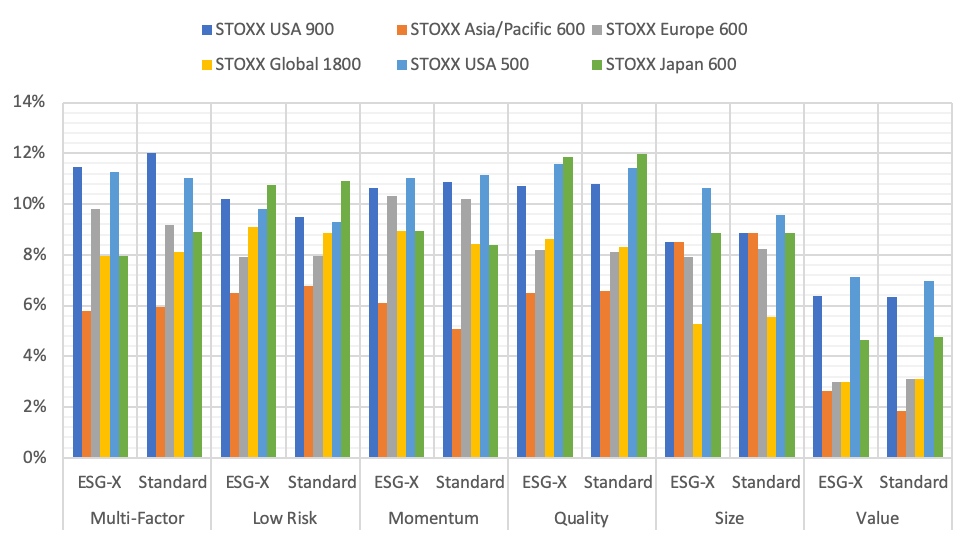

Despite the exclusions, the differences in the target factor exposures of standard factor and ESG-X factor indices are small. In fact, the ESG-X factor indices even harvest slightly more target risk premium than their standard factor counterparts in some cases (Exhibit 6).

Exhibit 6 – Total factor exposures of standard factor and ESG-X factor indices in STOXX Europe 600 universe

Conclusion

The STOXX ESG-X Factor Indices track the standard STOXX Factor Indices closely in terms of target factor exposure and performance. Based on our observations, there are at least two reasons for this. First, excluded stocks contribute only a small amount to the target factor exposures. Second, applying our methodology on a slightly narrower benchmark does not impede risk premia harvesting. Investors seeking both factor investing and ESG screens are able to do both without giving up performance.

1 For more information on the STOXX Factor indices see our research paper here and blog posts here and here.

2 The STOXX ESG-X Indices cover more than 40 geographies and were launched in 2019. For more information on them, visit a post here.

3 The STOXX Factor Indices also include Global ex USA variants.

4 Sustainalytics’ Global Standards Screening identifies companies that violate or are at risk of violating commonly accepted international norms and standards, enshrined in the United Nations Global Compact (UNGC) Principles, the Organisation for Economic Co-operation and Development (OECD) Guidelines for Multinational Enterprises, the UN Guiding Principles on Business and Human Rights (UNGPs), and their underlying conventions.